Get matched instantly

Why business lenders need your bank statements

Compare your matches and get the funding your business needs.

Totally free process and will not affect your credit rating

Instant Results

See how much you can borrow and with which lender, instantly

Up to $500k

For business loans, you could qualify to borrow up to $500,000

190+ Products

We offer over 190 products from more than 70 different lenders

You'll need to provide supporting paperwork when you apply for a business loan – no matter which type of loan and lender.

Big banks usually require complete financial statements, business plans and cashflow projections. But, non-bank lenders (also called alternative lenders) are more lenient and only need to see bank statements for the last six to 12 months.

Key points about why business lenders need to see bank statements

- Lenders ask for bank statements to verify your revenue and business cashflow stability — both prerequisites to service a loan

- Bank statements also show your overall business health

- The best way to submit bank statements is via direct data retrieval from your bank

- Non-bank lenders use technology to assess your business bank transaction data and credit profile

What do lenders look for in your bank statements?

Lenders will look at various bits of information on your bank statements to assess your loan eligibility. Firstly, they will check:

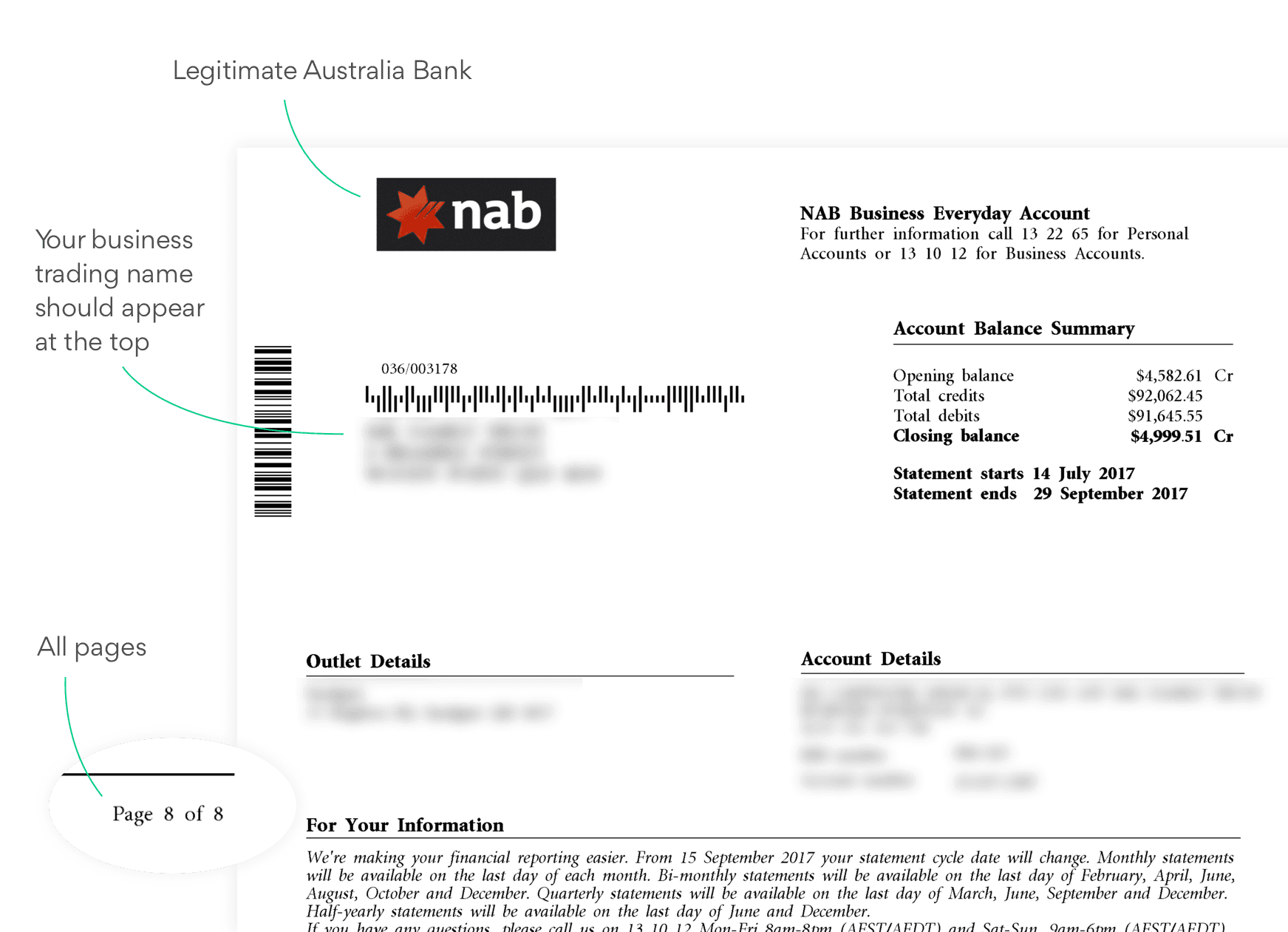

- You have an account with a legitimate Australian bank. The name of the bank should appear on every page of the statement.

- The statements are for your business account and not a personal account. Your business/trading name should appear at the top of the statement.

- You’ve submitted the entire statements . Lenders will check you haven't left any pages out or tampered with the statements to conceal information. Manipulating bank statements for official purposes is illegal and could get you blacklisted from borrowing.

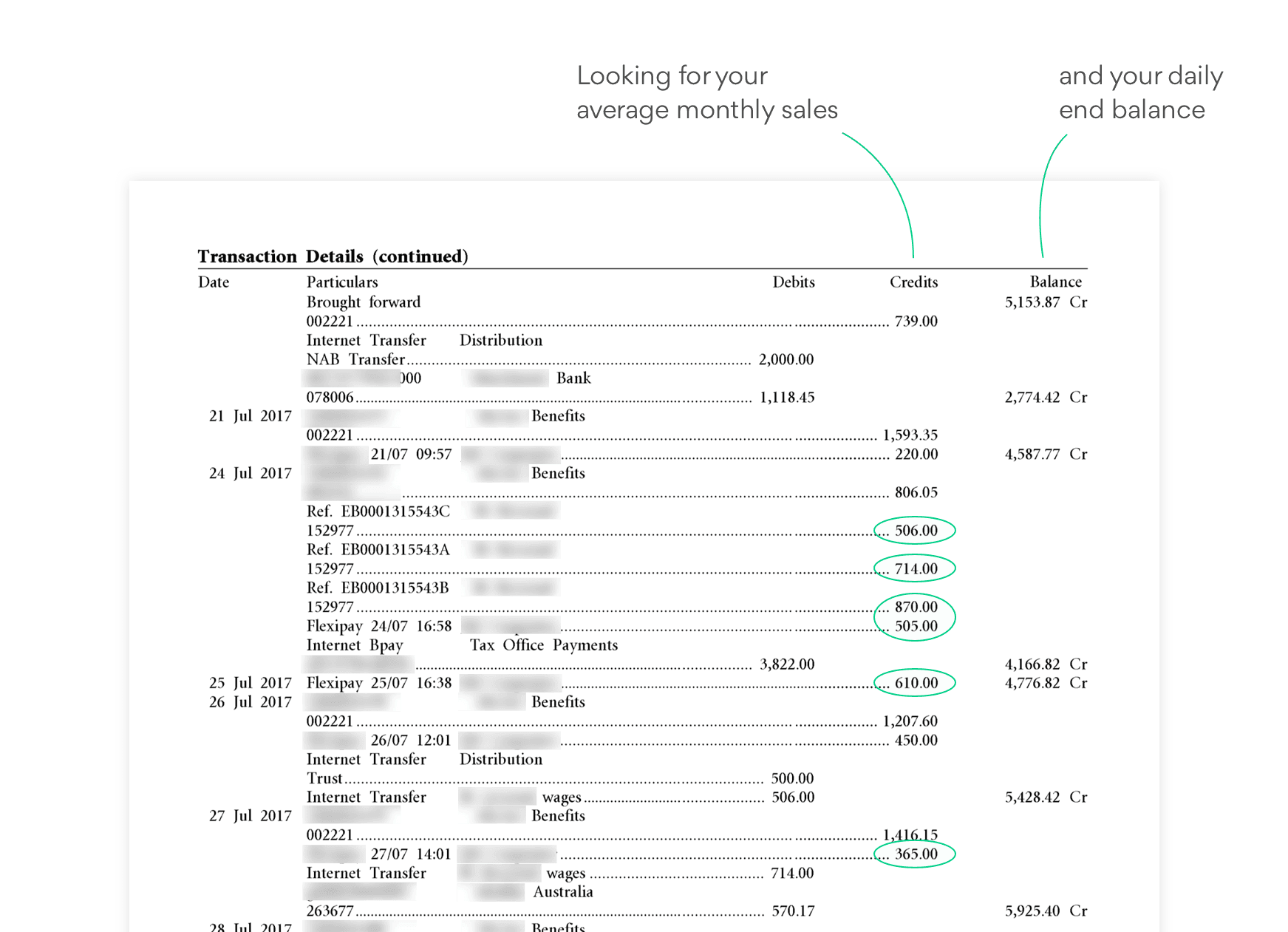

Secondly, they’ll look for evidence of your financial stability. The most important thing lenders will look at is your average monthly sales. This means they’ll be checking your deposits to determine your revenue. This will involve looking at any unexplained deposits, including cash deposits or transfers. Deposits that are not business income will be excluded from your average monthly sales.

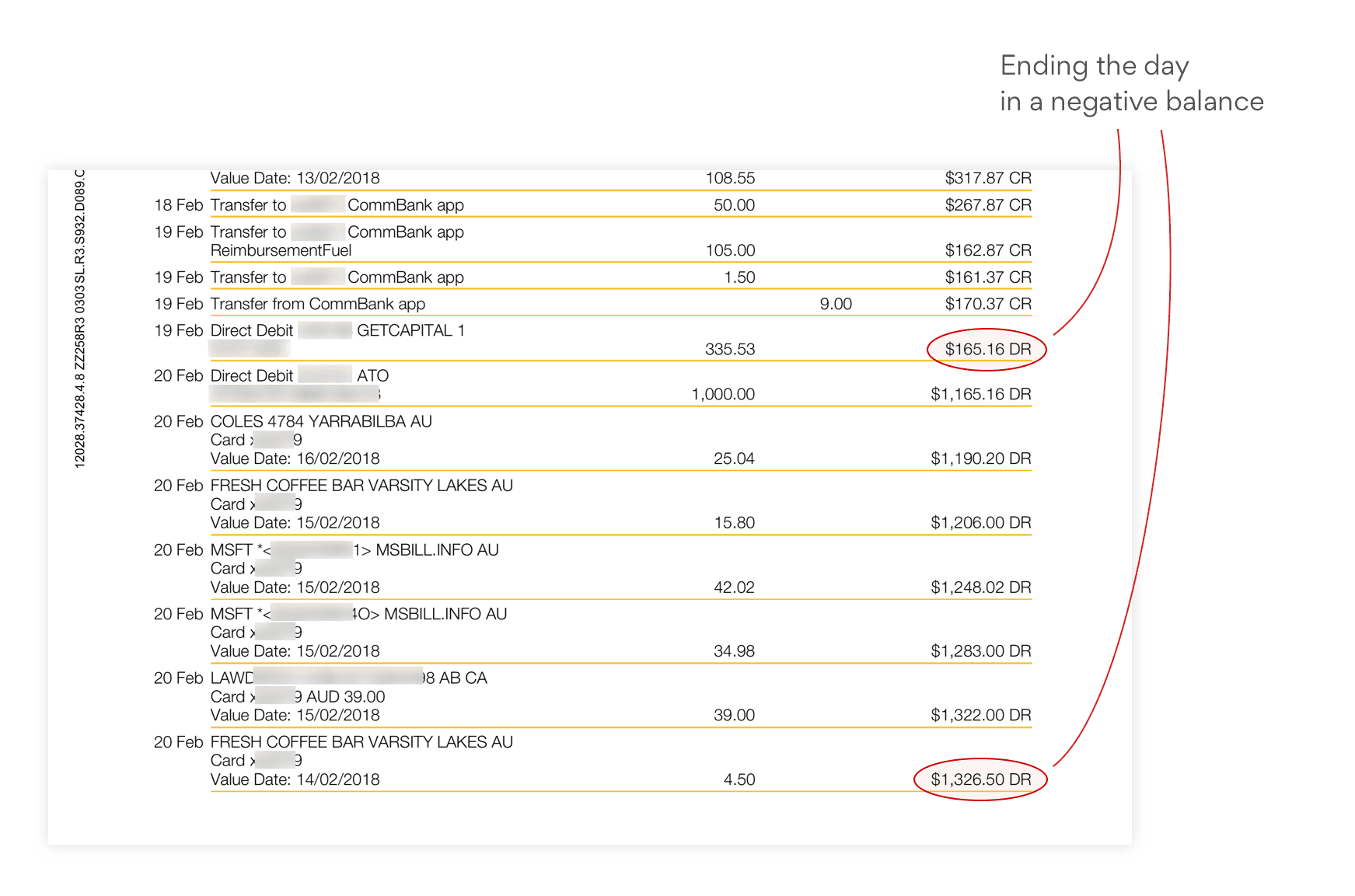

Lenders will also look at your daily end balance as a monthly average. This shows the lender how much surplus you have (on average) in your account on a given day. The following example graph shows the day’s closing balance, with some of them being negative.

What is considered a ‘healthy’ bank balance will vary between lenders and depend on the loan amount you’re applying for. The more you want to borrow, the higher the average and consistent balance they’ll want to see because they need to know you have enough funds to cover both your existing outgoings and the extra cost of your loan repayments.

Lenders will look for any negative days, dishonoured payments or unauthorised overdraft fees. A few mishaps may not prevent you from getting a loan, but multiple ‘adverse’ events in your payment history could impact your eligibility. This is a red flag to lenders as it suggests you may have problems paying them back, making you a risky borrower.

The next thing lenders will look at is the volume and frequency of your deposits. Are they all from one or two customers, or multiple? Regular deposits from multiple customers show that your income is consistent. If your business is seasonal or has fluctuating sales, they’ll need to see enough statements to show that you have a reliable income pattern. If you haven’t received deposits into your account for a few months, or if your deposit pattern has changed and suggests dwindling income, they may assume your business isn’t doing well and decline your loan application.

Finally, lenders will look for any recurring payments on debts or to creditors. This will include whether you make payments to other lenders. Having an existing loan won’t necessarily be an issue, but it could be a deal breaker for some lenders. If you do have existing debts, your potential new lender will need to know how much you’re paying each month and how much is still outstanding so they can assess your capacity to service their loan.

How to submit your bank statements

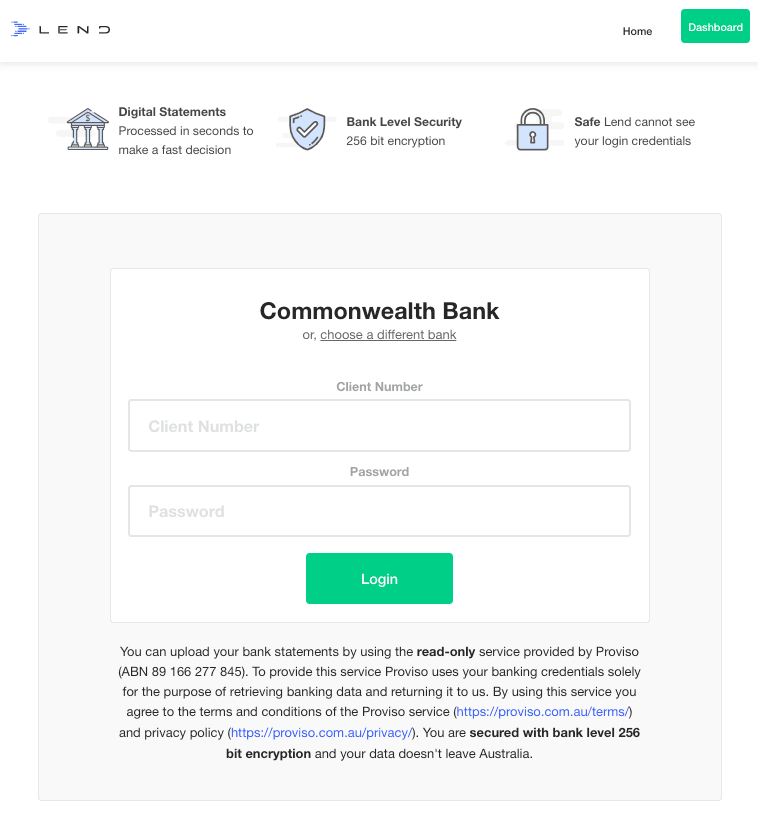

Most lenders will retrieve your bank statement data electronically directly from your bank with open banking or via a trusted third party like BankStatements.com.au (illion).

Here’s an example of how Lend uses BankStatements.com.au.

- You'll need to select your bank and log in to your online banking via our third-party platform to authorise illion to retrieve your bank statement data.

- illion will then retrieve a read-only copy of your bank statement data and send it to Lend.

- Lend's bank statement technology takes the raw illion data and rearranges it into an assessment, allowing lenders to see the necessary data points.

- The lender will assess your unique income sources, month-on-month revenue growth, number of related deposits per month, and percentage time in overdraft. The entire process is automated.

How to protect your financial data while applying for a loan

Australian banks and lenders must maintain the strictest data security standards under APRA's Prudential Standard Information Security (CPS 234). Lenders have stringent safeguards in place to protect their customer information, but there are always steps you can take to ensure you submit your data correctly during the application process:

- Don’t provide your online banking credentials over the phone or email. A legitimate lender will never ask you for your bank credentials in this way. They would only ask you to complete the process on their secure website.

- Check that the lender you’re applying with has a secure website. This goes for any website you use that requires entering personal, business or financial information. Look for the padlock in the browser. It means the website is using an encrypted connection.

If you’re worried about your information, you can always ask the lender what security they have in place to protect it. For example, which encryption protocol do they use? What information are they sharing with third-party partners?

You can always change your online banking password once the lender has retrieved your bank statements for extra peace of mind.