Get matched instantly

Inventory Finance

Compare your matches and get the funding your business needs.

Totally free process and will not affect your credit rating

Instant Results

See how much you can borrow and with which lender, instantly

Up to $500k

For business loans, you could qualify to borrow up to $500,000

190+ Products

We offer over 190 products from more than 70 different lenders

If your business sells products, you obviously need to buy inventory. But to buy merchandise you need cash, and sometimes that cash is tied up in what you already have sitting in a stock room or in what you’re acquiring. Inventory finance is designed to give businesses the ability to buy stock when paying with cash isn’t an option.

Key points about inventory finance in Australia

- Businesses can borrow up to 80% of their inventory’s liquidation value

- Interest rates on inventory finance can range between 10-20%

- Finance is secured against your inventory, not property or business assets

- Inventory financing repayment terms are shorter (1-6 months)

What is inventory finance?

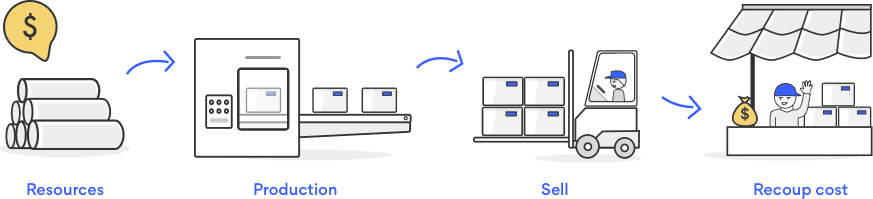

Inventory finance is a short-term business loan that uses your existing inventory or the stock you plan to buy as collateral for the loan. It’s a type of trade finance where the lender will advance you a portion of your inventory’s liquidation value and recoup costs when you sell that stock. Inventory or stock can include finished goods, parts or raw materials.

By offering stock as collateral for the loan, you’ll present less of a risk to a lender than with an unsecured business loan. This could help you secure a better interest rate or qualify for a loan with an imperfect credit score. If you default on the loan, the lender can reclaim any stock you haven’t sold to recoup costs. This is different from other small business loans, which typically require property or equipment as security.

Inventory finance is especially popular with businesses with large quantities of stock on hand, like manufacturers, wholesalers, retail shops, restaurants, car dealerships, etc.

Pro tip: You can typically only use an inventory loan to buy stock, but some lenders may allow you to use the funds for other business purposes. You can alternatively consider a bridging loan.

How does inventory finance work?

Inventory finance comes either as a term loan or a line of credit.

Inventory term loan: You get a lump sum of money that you repay in fixed monthly payments over a set period (called the term). In most cases, your stock will be the only collateral for your loan. You can use existing stock or pledge the inventory you plan to buy with the loan. The shorter the term, the less you’ll pay in interest, so it makes sense to tie it to your anticipated stock turnaround.

Inventory line of credit: You get an at-call credit facility you can access anytime to purchase inventory (up to an agreed limit). In this case, the lender pays your supplier for the inventory you need and you make repayments when the inventory is sold. When you need more inventory, you simply continue drawing on the line of credit and it doesn’t strain your cashflow. This is sometimes known as ‘floorplan finance’ and is more commonly used for big-ticket items like cars or appliances.

Who’s eligible for inventory finance?

There are several criteria your business will need to meet to qualify for inventory finance:

- An active ABN or ACN. You must operate a business registered in Australia.

- Trading history of six to 12 months. Your time in business is a big factor. Banks usually require a longer operating time than non-bank lenders.

- Show a track record of successfully selling inventory. You’ll also need a credible valuation of the stock.

- A steady turnover to repay the loan. Be prepared to provide bank statements and tax returns.

- A good credit score. The minimum credit score for business lending is around 400. Some lenders may be willing to work with you even if your credit record isn’t spotless, but you can expect to pay more for your finance.

Lenders will also pay particular attention to the industry in which your business operates. You may struggle to obtain finance if your sales are highly seasonal and your earnings are cyclical, or if your stock consists of mostly perishable goods or items that can quickly become obsolete (like technology). However, several lenders specialise in particular industries, so do your homework and look for a lender who is a good fit for your business.

How much can you borrow with inventory finance?

In most cases, you’ll only be able to borrow a proportion of the stock’s value (up to 80%), not the full amount. You may be able to borrow up to $5 million against your inventory, but this will depend on your inventory’s liquidation value, sales turnover and the lender’s assessment of your business.

What to consider when taking out inventory finance

Interest rates

Rates typically range from 10–20%, depending on the type of stock used as collateral and your business credit profile. They may be fixed or variable, depending on the lender.

Fees

Most lenders charge a set-up fee, and some may apply ongoing charges, especially for revolving facilities or lines of credit. Make sure you understand what fees apply and how often they are charged.

Repayment terms

Terms usually range from 1–6 months or longer, depending on the lender and the structure of the facility.

Terms and conditions

As with any form of business finance, review the agreement carefully and seek advice if needed before committing. Where possible, build flexibility into the repayment structure so you have a buffer if sales fluctuate.

Pro tip : Whichever option you choose, be confident you can sell the inventory within the agreed timeframe. If not, you could end up with unsold stock and a loan still to repay. Suitable insurance cover is also important to protect against theft, loss, or damage.

Pros and cons of inventory finance

Pros | Cons |

|---|---|

|

|

When to use inventory finance

Here are some common scenarios when businesses can use inventory finance.

- Prepare and stockpile inventory for busy seasons. Businesses that experience seasonal fluctuations in demand for their products may use inventory finance to bridge the gap between production and peak sales periods. This ensures they have enough inventory to meet customer demand without tying up too much of their working capital.

- Bulk purchases. When a business has the opportunity to purchase inventory in bulk at a discounted price, inventory financing can help cover the upfront cost. This can lead to cost savings in the long run.

- Inventory management. Inventory financing can also be used to improve inventory management by allowing a business to liquidate slow-moving or excess stock and reinvest in more profitable products.

- Expand product lines. When launching a new product or expanding existing product lines, a business may use inventory finance to build up stock levels before the product hits the market. This ensures they can meet initial demand without straining their resources.

- Cover short-term cashflow shortages. Businesses facing temporary cashflow challenges may use inventory financing as a short-term solution to cover operational expenses while waiting for payments or invoices.

- Keep up with customer demand (and increase sales) . Inventory finance can help businesses avoid running out of stock and ensure they have enough inventory to meet customer demand.

- Payment schedules disrupt your business' inventory levels. Companies that offer payment terms to suppliers or customers may struggle with cashflow and stock levels and could use inventory finance to bridge that funding gap.

Inventory finance example

Let’s consider an example based on a fictional company called…

Company name : FitActive Sportswear

Industry: Retail (activewear)

Loan amount: $30,000

Case: FitActive Sportswear is a growing retail business specialising in activewear, including athletic apparel, fitness accessories, and sportswear for men and women. The business operates both online and through a physical store.

The activewear industry experiences seasonal fluctuations, with increased demand during the spring and summer months due to outdoor activities and fitness trends.The business needs to maintain a diverse inventory with a wide range of sizes, colours, and styles to cater to customer preferences. This requires a significant investment in stock.

FitActive Sportswear applies for an inventory loan of $30,000 to secure additional stock, based on its existing inventory's assessed value and projected inventory needs for the upcoming season.

By using inventory financing, the retail business can optimise its inventory levels, take advantage of supplier discounts throughout the year and maintain a steady cashflow. FitActive Sportswear then repays the loan in full without penalties and improves its creditworthiness in the process.

*Fictional case study

How to apply for inventory finance

To apply for inventory finance, you’ll need to provide financial documentation, an up-to-date inventory list and information about your business.

1. Financial documents

You’ll need to provide some financial documents to show the lender you can service the loan even if you don’t sell your inventory on time.

- Bank statements from the last six to 12 months

- Business registration and tax information (e.g. BAS statements, tax returns)

- Personal tax returns for sole traders

If you’re borrowing more than $100,000:

- Balance sheets

- Profit and loss (P&L) statements

2. Inventory paperwork

Your lender will also want to evaluate your inventory’s value and sales forecasts.

- Current and previous inventory list

- Inventory turnover records, which show the frequency and value of stock you’ve sold

- A realistic sales forecast to show the lender what you plan to achieve and how soon you’re likely to be able to repay your loan

3. Business information

Lastly, you’ll be asked to provide information about your business trading history and current model.

- Your business structure (e.g. company, partnership, joint venture, sole trader)

- The location of your business

- The industry your business operates in

- Identification documents (e.g. driver’s licence, passport)