Get matched instantly

Merchant cash advance loans

Compare your matches and get the funding your business needs.

Totally free process and will not affect your credit rating

Instant Results

See how much you can borrow and with which lender, instantly

Up to $500k

For business loans, you could qualify to borrow up to $500,000

190+ Products

We offer over 190 products from more than 70 different lenders

A merchant cash advance or merchant finance can help your business secure immediate funding by leveraging future credit and debit card receivables.

Key points about merchant cash advance loans

- The median amount requested for a merchant cash advance is $20,000, according to Lend proprietary data

- Merchant cash advance rates range from 5-20% of daily card sales

- Short-term financing, usually up to 24 months

- A merchant cash advance doesn’t impact your credit score

- Merchant finance is available from select specialist lenders

What is a merchant cash advance?

A merchant cash advance (MCA) or business cash advance is based on your card sales revenue. This alternative type of business finance allows you to borrow money (usually a lump sum), which you repay as a percentage of future credit card and EFTPOS sales, plus a small fee.

Under this short-term loan agreement, the lender purchases your future transactions and advances you payment against your future sales. It doesn't have a fixed repayment schedule and, therefore, doesn't impact your credit score.

A merchant cash advance is ideal for businesses with a high turnover in card sales, such as retail shops, cafes and restaurants. This includes point of sale (POS) card terminals and online payment gateways (excluding PayPal).

How does a merchant cash advance work?

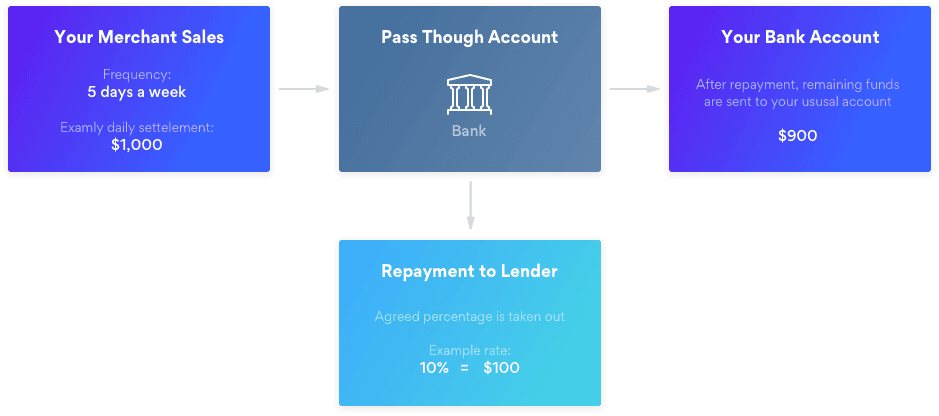

If you're approved for a merchant cash advance, you'll receive a lump sum from your lender, usually by direct deposit into your bank account. In exchange, a fixed percentage of your daily credit card and EFTPOS sales will be deducted until the cash advance is paid back in full. This happens automatically through your merchant account.

The agreed percentage of your card sales is repaid daily or weekly, depending on the financing terms. The percentage you pay back is known as the 'holdback' or 'retrieval' rate and can be anywhere between 5-20%. Here's a visual example of how it works.

Merchant cash advance repayments & terms

With a merchant cash advance, you pay back a fixed percentage of your daily card sales. Therefore, your repayments will vary based on your card sales revenue. However, you'll still need to agree on a term with the lender (usually between 1 to 24 months). If it includes a renewal feature, you can negotiate the amount and term once you've paid back a certain amount.

Merchant cash advance pros & cons

Pros | Cons |

|---|---|

|

|

Who’s eligible for a merchant cash advance?

Eligibility requirements for a merchant advance are more straightforward than those for a traditional loan. You need:

- A business registered in Australia (i.e. active ABN or ACN)

- A trading history of at least six to 12 months

- A merchant account (business bank account that accepts debit and credit card transactions)

- Minimum monthly card sales

One of the main benefits of a business cash advance is that you don’t need a perfect business credit score to get approved because the lender is taking money from your sales before you get paid.

How much can you borrow with a merchant cash advance?

According to Lend proprietary data, the median amount for a merchant cash advance in Australia is $20,000. However, each lender will have a minimum and maximum amount — typically ranging from $5,000 to $500,000. Your borrowing capacity will depend on your merchant sales history and business finances. Merchant cash advance lenders can advance up to 70% of your average monthly sales through your merchant account (sometimes more at the lender's discretion).

Merchant cash advance loans often have a renewal feature. Once a certain amount has been paid off you can borrow again, before paying the full amount back. For example, if your MCA has a 50% renewal program, you’ll be eligible to renew for additional funding after your payback is 50% complete.

How to apply for a merchant cash advance

The application process for a merchant cash advance can be completed entirely online. The lender will want to see that you have enough revenue through card payments and good cashflow. They will determine your borrowing capacity by looking at:

- Your average monthly merchant sales

- The number of merchant deposits

In most cases, you won't need to provide the usual loan application paperwork like business financials, tax returns or BAS statements. However, this will depend on the amount you borrow and the lender.

Your application could be approved within 24 hours, and the funds accessible within 1-2 business days.

What can you use merchant finance for?

According to proprietary Lend data, the most common purposes businesses use merchant finance in 2023 include:

- Other (e.g. marketing, inventory): 40%

- Start a business: 21%

- Day-to-day capital: 19%

- Expansion: 8%

- Buy an existing business: 6%

- Renovations: 5%

Who’s a merchant cash advance suitable for?

Merchant cash advance loans are typically used by businesses with a high volume of daily EFTPOS transactions like retail shops, cafes, restaurants, health and beauty stores, etc. This type of financing is also suitable for businesses that need working capital to cover seasonal cashflow fluctuations.

How does a merchant cash advance compare to other loans?

Loan | Requirements | Interest rate range | Terms |

|---|---|---|---|

Merchant cash advance | ID check 6+ months in business Minimum monthly card sales No collateral | 10-20% of daily card sales | 1-24 months |

Secured business loan | Credit & ID check Bank statements 6-12 months in business Business financials Collateral (e.g. property) | 10-15% p.a. | 1-10 years |

Unsecured business loan | Credit & ID check Bank statements 6-12 months in business No collateral | 15-20% p.a. | 1-3 years |

Business line of credit | Credit & ID check Bank statements Good credit score 6-12 months in business No collateral | 10-15% p.a. on what you draw | 3-30 months |

FAQs about merchant finance

The main difference between a merchant cash advance and a business loan is the repayment structure. A merchant cash advance has no set repayment terms and is repaid as a percentage of daily card sales. In contrast, a small business loan has fixed weekly or monthly repayments with interest. Additionally, business loans are typically secured against an asset.

A merchant cash advance is similar to an unsecured business loan, meaning you don’t need to provide collateral (e.g. property or other assets) as security. Instead, your future card sales are the guarantee.

Non-bank and select specialist lenders offer merchant cash advances and some banks may also offer some MCA facilities. Some popular merchant cash advance providers in Australia include Finstro, Biigga and Capify Australia.

Yes, you can still get a merchant cash advance if you have adverse credit, as long as your business meets the minimum eligibility requirements and has enough revenue through card payments. This will depend on your specific circumstances, and approval is at the lender’s discretion.

Sources:

1. Proprietary data of small businesses that applied for a merchant cash advance through Lend.com.au and have been operating for at least five years (2023).