Top 10 reasons for

business failure

(and how to avoid it)

Compare your matches and get the funding your business needs.

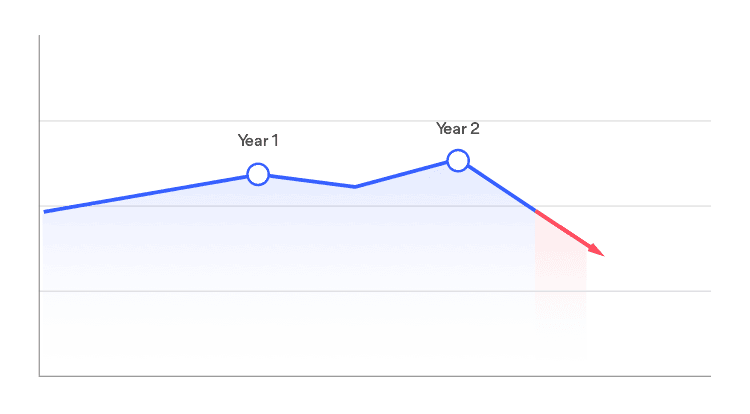

Picture this.

You have your business up and running and everything is looking great.

Year one passes, and you’ve turned a profit. Year two goes pretty well too.

But year three isn’t quite as kind. You have to let some employees go to cut costs. You take out finance to boost your working capital but end up heading deeper into debt. Eventually, you reach the point of no return and you have to close down.

That’s not the vision you have for your business. It’s not the vision any entrepreneur has when they start out – but the sad truth is:

Small business failure is all too common.

I’m not trying to get you scared here. It’s just that forewarned is forearmed – the more you know about why small businesses fail, the better equipped you’ll be to avoid running into trouble.

At this point, you may be wondering:

“Just how high is the risk of business failure?”

Let’s take a look.

Small business failure – what do the stats say?

First off – what exactly do I mean by ‘small business’?

Here are the official definitions:

ABS (Australian Bureau of Statistics) : A business that employs fewer than 20 people.

ASIC (Australian Securities and Investment Commission) : A business with an annual revenue of less than $25 million, fewer than 50 employees, and less than $12.5 million in consolidated gross assets.

ATO (Australian Tax Office) : A business with less than $2 million in annual turnover revenue.

Fair Work Ombudsman Australia : A business with fewer than 15 employees.

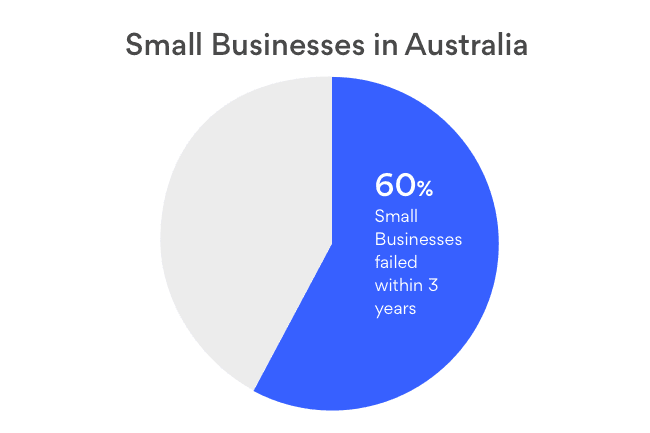

In fact, approximately 97% of businesses in Australia are considered to be small businesses. And using just the ABS definition of a small business, an estimated 60% of small businesses fail within the first three years.

Yep. I said 60%. Within three years.

That’s an alarmingly high number when your business could end up among them.

So, what goes wrong?

The top ten reasons small businesses fail

1. Not having enough start-up capital

If you don’t have enough money behind you when you start up your business, you can end up with all sorts of hassles.

It can take up to two years for a business to really take off. During that time, you’ll face an endless stream of expenses – most of which you won’t be expecting.

If you haven’t researched how much money you’re going to need to set up and keep your business afloat for those first few years (without relying on the luxury of profits!) you may find yourself running out of money before you even gets a chance to succeed. This start-up calculator can help you predict how much you’ll need.

If you don’t have a lot of capital to fall back on, you’ll need to line up finding to tide you over until red turns to black and your business starts paying its way. There are several ways to fund your start-up – investors, loans or even crowdfunding – but if you end up deciding to borrow, remember you’ll have to cover loan repayments too, which means you’ll need even more money from month to month.

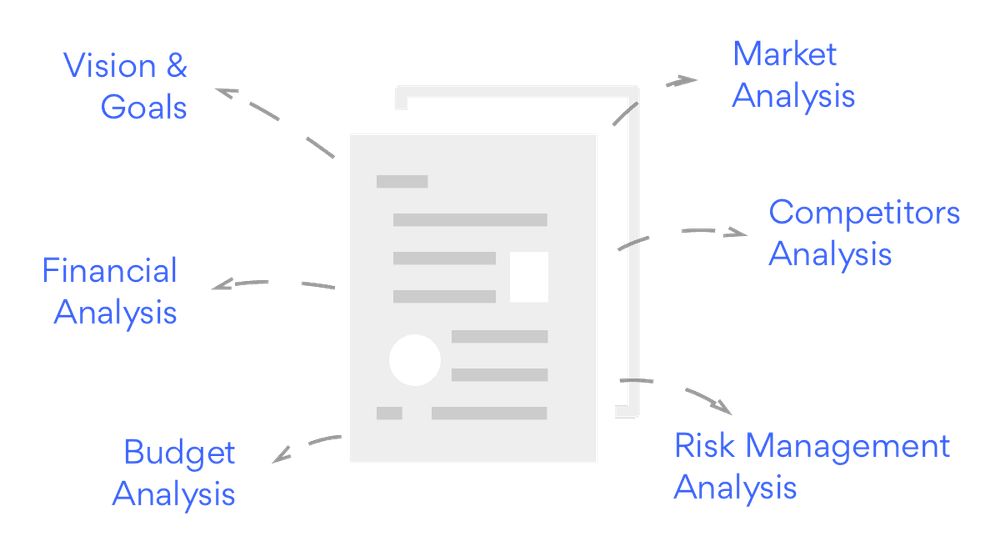

2. Lack of proper planning and research

Starting out in business is like taking a long trip into unknown territory. Before you start, you need a map, or you’ll soon get very, very lost.

With a new business venture, your business plan is your map. If you’re going to have any chance of commercial success, you’ll need a solid business plan in place from the outset. A plan that you, your business partners and your staff all understand, so that everyone is on the same page.

You’ll need to cover:

- Your vision and goals

- Financial needs analysis and budget, including cash flow projections, income statement, sales projections, expense forecasts, and capital equipment and supply lists

- Market and competitor analysis

- Analysis of potential problems and strategies to fix them

To keep your business on track you’ll need to review and update your business plan regularly.

As for research, make sure you know how much demand there really is for your products or services. What do your customers really need? Will your products or services really benefit them more than your competitors’ – and if so, how can you prove it?

If you need a bit of help with the planning and research, check out this advice from Business Basics.

3. Lack of proper training

If you’re running or about to set up a business, you’re probably an expert in your field of operations. You may be an accountant or an engineer, a florist or a software guru. That’s great news for your customers, who’ll soon be relying on your expertise – but it doesn’t necessarily mean you’re equipped to run a business.

The thing is, if you don’t have the proper skills and training in how to run a business, the odds are you’ll get caught up in the day-to-day work. And while you’re flat out with that, you won’t have time to focus on the big picture and strategic thinking that’s vital to your long-term success.

So, are you ready to run a business?

Ask yourself if you:

- Know how to analyse and manage your financial performance

- Have the skills to write a business strategy and keep your business on track

- Know how to market your business for maximum profit

- Feel confident managing staff

If the answer to any of those questions is no, don’t worry. There are plenty of places you can turn to learn the skills you need to run a successful business. And, of course, you can always seek professional help.

4. Poor financial management

So your business is open, you’ve secured enough capital to maintain the business while it takes off, but you discover you aren’t very good at actually managing the money.

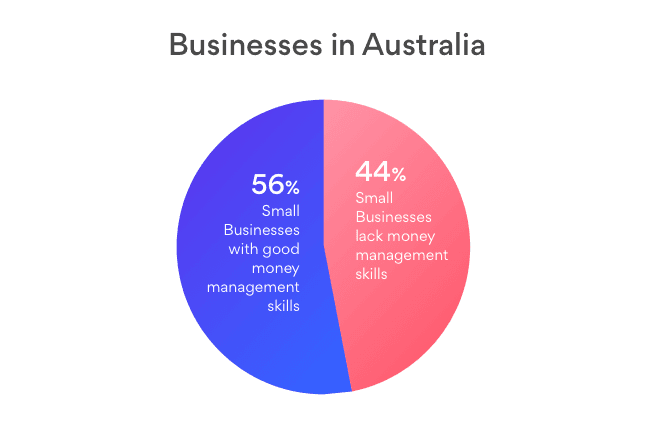

According to ASIC, a staggering 44% of small businesses lack basic skills in money management.

If you don’t feel comfortable or knowledgeable enough to maintain your own funds, get someone on your team who is! At the very least, hire a great accountant to keep you from making financial decisions or errors that could cost you your business.

5. Poor debt management

If you offer credit terms to your customers, there’s always a risk that they won’t pay on time (or at all).

No matter how profitable your business is on paper, you could easily run into a cash flow crisis if too much of your working capital is tied up in bad debts. And running out of cash is the fastest of fast tracks to business failure.

You need to have a strategy in place to handle slow-paying customers, including iron-clad contracts and a dedicated person (or external company) to chase up payments.

6. Poor record keeping

If you can’t answer the question ‘How are we doing right now?’, then the chances are you don’t have adequate records. If you’re going to make sound strategic decisions about your business, you’ll need to have up-to-date information at your fingertips about your sales performance, your financial position and your cash flow.

If record-keeping isn’t your strength, hire someone to take care of your weekly and monthly financial reports, tax documents, sales records and debt ledgers – and make sure they keep you in the loop so that you’ll know what changes you need to make before it’s too late.

7. Being in business for the wrong reason

It takes hard work and drive to lead a business to success. Unless you have a clear vision of what you want to achieve, and are absolutely certain about your ‘why’, you may just find yourself running out of steam along the way.

Make sure that you – and all the people who are in this with you, including your management team and any investors – share your vision and are working towards the same goals.

8. Depending on single customer

I’m sure you’ve heard the expression ‘don’t keep all your eggs in one basket’.

It couldn’t be more relevant when it comes to small business. While it’s great if you have a loyal customer throwing you so much work that you’re working close to capacity – what happens if they suddenly drop you, and you’re left without that income?

If you find yourself in this position, you need to act fast to mitigate the risk. That means finding a way to bring in more customers. It might just be a matter of marketing or trying new sales channels – or you may have to diversify your offerings to meet customers’ needs.

9. Growing too quickly

It can be exciting to see the revenue flowing and the customer base growing – but it’s vital that you manage that growth sustainably. Overstretch, and all too soon you could end up closing your doors.

Be wary of making big financial decisions or pursuing a growth opportunity (like expanding to new premises or buying out a competitor) without careful analysis – especially if you’ll need to take out a loan to finance it. Be sure, first, that you’ll be able to generate enough extra profit to cover the additional costs – and that it will happen before you hit a cash flow crisis.

10. Location

If you’re relying on foot traffic to keep customers flowing to your door, you’ll need to base your business somewhere they can easily find you.

But prime locations command premium rents, and as a newcomer your income might not cover that kind of expense. You’ll need to do some pretty careful research to find an affordable location that will still bring you in enough business.

If yours isn’t a retail business, avoid splashing out on expensive offices in the precarious start-up stage. After all, the lower your overheads, the quicker you’ll start making those elusive profits.

These aren’t the only ways a business can fail, but they top the list.

I’ve shared quite a few insights on how to avoid those specific pitfalls.

Here are some more.

Six more ways to keep your business afloat

Invest in the right resources

Resources include partners or advisors to help you run your business, equipment and technology, and marketing tools.

If you’re going to keep up with your competitors (or better still, leave them in the dust), you’ll need a first-rate management team, robust equipment and technology, strong internal systems and a knock-out marketing strategy.

And then there are your people. Any business, big or small, needs skilled and dedicated employees who are enthusiastic and customer-oriented. Hire the best you can afford, and treat them so well they never want to leave.

Manage your cash flow

I can’t stress this enough:

CASH IS KING.

Even household names like Dick Smith end up on their knees when the cash runs out. Turnover means nothing if your expenses are through the roof. Profits are irrelevant if all your cash is tied up in stock or unpaid invoices.

If you can’t pay your bills when they fall due, you’re on the path to disaster, so the one thing you need above all else is an up-to-the-minute picture of your cash flow situation.

Arm yourself with accurate cash flow projections, so you’ll see problems coming and have time to fix them.

Know what your customers really want

With so much potential competition out there, you need to find out what problems your customers face, what they need, and what they’d pay even more to have.

Keep your eyes on the market and watch out for disruptive new products or services that could lure your customers away. Look for unique or creative ways to delight them, and never underestimate the impact of great service when it comes to building customer loyalty.

Get online

90% of customers now search online before they make a purchase.

They’re looking for great deals and the best prices – but they’re also checking out your credibility, especially if you’re offering professional services.

If you’re selling products, a website can help you extend your reach and capture customers in whole new markets. If you’re selling expertise, your website is your showcase – the place where you can prove yourself as a thought leader in your industry.

Consider using social media to build social proof – genuine customer reviews and recommendations that will carry far more weight than a testimonial on your website (let’s face it, no one believes you didn’t just write those yourself).

Marketing, marketing, marketing

If you want to grow, you have to get out there. I really can’t overstate how important marketing is for your business.

There are many ways to go about it though – think traditional media vs social media, paid advertising vs content marketing – so you need to start with a marketing plan.

If all this sounds like a foreign language, don’t despair. There are loads of great agencies out there who can help you create your marketing strategy, brand your business, set your budget and launch a killer marketing campaign.

Ask. For. Help.

To succeed in business, you need to know your strengths – and your weaknesses. Financial management and taxation, laws and regulations, marketing, business strategy – you can’t possibly be an expert on everything, so find people to help you fill the gaps in your knowledge.

Meet with experienced strategists, find a mentor, hire financial and legal advisors, bring a marketing guru onto your team.

The fact is that nothing beats sitting down with someone who has hands-on experience – so if you’re not sure how to do something, don’t be afraid to ask someone who’s already done it.

Conclusion

The best way to steer your business onto the right path – and keep it there – is to arm yourself with knowledge.

- Understand the main reasons why businesses fail and what you can do to prevent them

- Learn how to avoid the common pitfalls that bring as many as 60% of small businesses crashing down

- Be honest about what you know and don’t know and take training (or hire advisors) to fill the gaps in your skills

- Surround yourself with people who can complement your strengths and balance your weaknesses

With proper planning, research and training, the right resources behind you and people around you, you’ll be well on the way to business success.

And if you ever find yourself among the 60%, remember that many successful entrepreneurs have a few failed ventures in their past. The key is to learn from mistakes – both your own and other people’s – and find out everything you didn’t know last time, so you’re ready to get back out there and achieve your dream.

Do you have any insights to help new business owners get on the path to success? Share your comments below.

Get Your Competitive Quote Today

This process will not affect your credit rating in any way.